Sundry Photography

In our previous protection of Analog Gadgets, Inc. ( NASDAQ: ADI), we took a look at the business’s acquisition of Maxim Integrated and its ramifications for ADI’s service. First of all, the acquisition strengthened ADI’s position in the Analog market by contributing 29.5% of the combined business’s incomes and increasing its market share from 9.2% to 12.8%, simply behind Texas Instruments ( TXN) at 19.6%. Second of all, we expected that ADI’s combination of Maxim’s power management incorporated circuit (‘ PMIC’) would allow the expedition of semiconductor chances in health care. Last but not least, we anticipated that the synergy in between ADI and Maxim would cause enhanced revenue margins.

In this analysis of Analog Gadgets, we look into the considerable effect Maxim had on ADI’s profits development, which reached a remarkable 64.2% in 2022, exceeding our preliminary projection of 37% development. First of all, we take a look at the modifications in market share within the analog market considering that our previous protection, particularly concentrating on the space in between ADI and Texas Instruments (TI). Next, we recognize the sectors where Maxim’s impact surpassed our expectations. Furthermore, we examine the effect of Maxim on revenue margins compared to our earlier forecasts. Last but not least, we evaluate the brand-new item releases from the previous 6 months and compare them with the preceding 6 months to identify if the development arising from the acquisition can be sustained through a constant stream of item developments. Based upon this details, we supply an upgraded profits and margin outlook for the business.

Joint Analog Market Leader with Texas Instruments

IC Insights, Business Data, Khaveen Investments

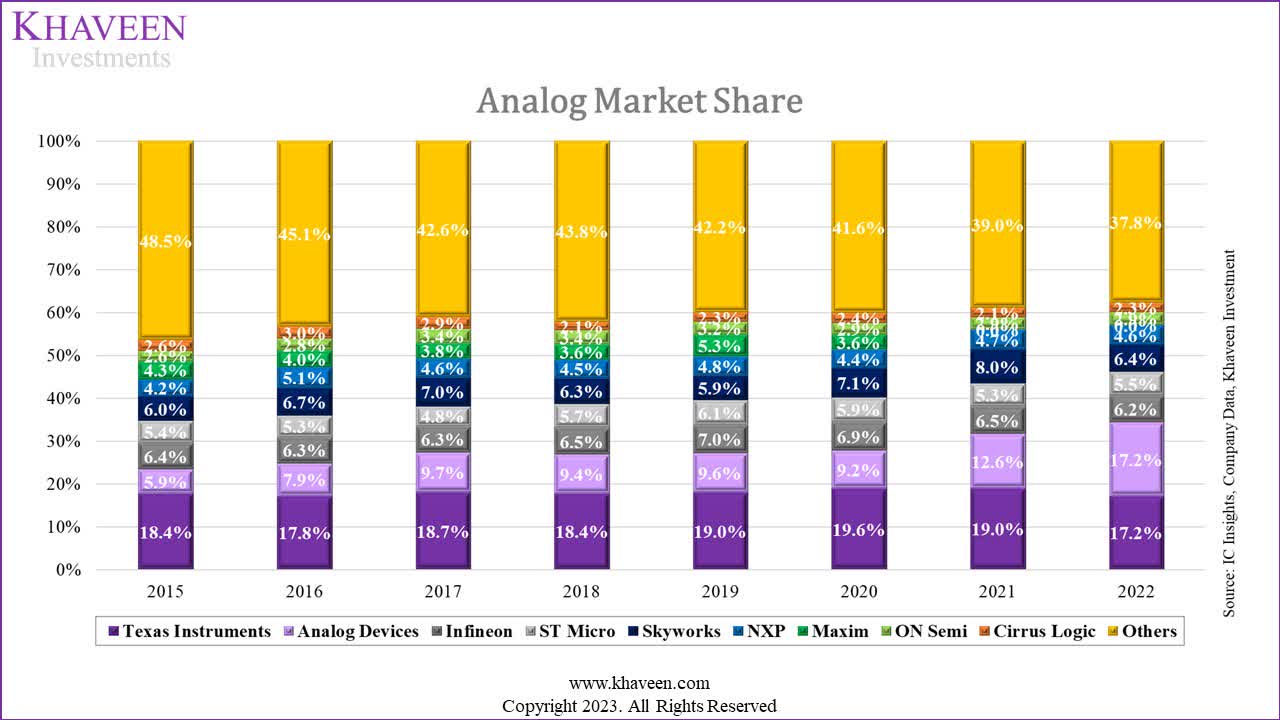

In the chart above, we determined the analog market share in 2021 by taking each business’s analog incomes supplied by IC Insights and dividing that by the overall analog market profits supplied by WSTS We approximated the 2022 analog market share by forecasting each business’s incomes (other than TI) based upon its latest fiscal year development rate and once again divided by the analog market profits supplied by WSTS. For TI, we got its 2022 analog profits straight from its yearly report.

ADI’s market share in 2021 (12.6%) was reasonably in line with the combined market share of ADI and Maxim in 2020 (12.8%). Nevertheless, our anticipated analog market share in 2022 programs that we anticipate ADI to have actually gotten substantially, with its market share anticipated to increase by 4.6% to reach 17.2% in 2022, joint greatest with TI. Our company believe ADI to have actually gotten that market share from TI, Skyworks ( SWKS), and the Others, who all lost one of the most.

TI would have had a decrease in market share as its analog profits development was just 9.32% in 2022, lower than the marketplace development of 20.8%, whereas ADI grew 64.2% in 2022. Furthermore, according to MarketWatch, automobile semiconductor sales are the “sole development chauffeur” for analog semiconductors due to the decline in the semiconductor market. Texas Instruments automobile profits grew 30% in 2022 whereas ADI’s automobile sector grew by 101.5%. We likewise think Skyworks to have actually lost 1.6% of its market share, which is a big piece of its 2021 market share (8.0%) due to its general profits development likewise being listed below market development at 7.4%. Our insights from the analog market share chart from 2015 to 2022 are as follows:

- ADI has actually regularly increased considering that 2015.

- TI has actually been steady over the previous 8 years however dropped to its most affordable level ever in 2022.

- Smaller sized rivals have actually been reasonably flat.

- Other little business have actually reduced their market share.

In conclusion, our company believe ADI has actually reached end up being the joint market leader together with TI with a 17.2% market share in the analog market in 2022. This was a mix of TI’s analog sector growing lower than the marketplace in combination with ADI growing above the marketplace. We anticipate ADI to acquire market share in the coming years as it is pursuing the best method to run in the Analog market, and this is shown by it being the only business to regularly acquire market share considering that 2015, whereas the marketplace share of its rivals has either stayed flat or reduced. Listed below, we will evaluate the factors behind ADI’s impressive development in 2022 and identify if Maxim played a part in increasing incomes above expectations.

Development Driven by Maxim Acquisition

|

Profits by Section ($’ 000s) |

2019 |

2020 |

2021 |

2022 |

5-year Typical |

Our Previous Analysis 2022 Projection |

|

Industrial |

3,003,927 |

3,005,585 |

4,026,909 |

6,069,332 |

||

|

Development Rate % (YoY) |

-4.0% |

0.1% |

34.0% |

50.7% |

23.1% |

|

|

Automotive |

933,143 |

778,714 |

1,248,169 |

2,515,513 |

||

|

Development Rate % (YoY) |

-7.6% |

-16.5% |

60.3% |

101.5% |

34.2% |

|

|

Communications |

1,284,087 |

1,193,809 |

1,206,867 |

1,880,697 |

||

|

Development Rate % (YoY) |

11.5% |

-7.0% |

1.1% |

55.8% |

17.6% |

|

|

Customer |

769,908 |

624,948 |

836,341 |

1,548,411 |

||

|

Development Rate % (YoY) |

-17.6% |

-18.8% |

33.8% |

85.1% |

11.4% |

|

|

Overall Profits |

5,991,065 |

5,603,056 |

7,318,286 |

12,013,953 |

9,788,075 |

|

|

Development Rate % (YoY) |

-3.8% |

-6.5% |

30.6% |

64.2% |

20.6% |

33.7% |

Source: ADI, Khaveen Investments

The business’s profits grew by 64.2% in 2022, greater than the 5-year average of 20.6% and our projection of 33.7%. Although all sectors grew above 50%, the one that stands apart is the automobile sector which grew at 101.5% (20.9% of 2022 profits). Industrial, 50.5% of 2022 profits, grew at 50.7% and contributed 43.5% to profits development, the biggest among all sectors. Based upon its yearly report, management associated the impressive development to the “acquisition, which contributed roughly 65% of the boost in overall profits year over year”. For that reason, we determined that 41.7% of ADI’s 64.2% development in 2022 is straight credited to Maxim with the staying 22.5% of the development credited to ADI’s natural development, which is much greater compared to our anticipated natural development of 6.64% from our previous protection

We anticipated ADI to take advantage of combination with Maxim in regards to semiconductors in health care (commercial sector), nevertheless, we did not take into consideration the advantage of Maxim’s items for ADI’s automobile sector. In its Q4 2022 profits rundown, the CEO of ADI, Vincent Roche formerly mentioned that the business’s “development in Automotive was underpinned by battery management systems”. In relation, taking a look at the Q4 2021 profits rundown, the business highlighted its BMS position being supported by its Maxim acquisition.

Our BMS position is additional reinforced with Maxim, we now offer to 7 of the leading 10 EV producers, and our increased innovation and item scale allows us to attend to brand-new SAM … … Maxim’s strong and growing power management abilities match our portfolio.– Vincent Roche, CEO

For that reason, ADI’s automobile BMS portfolio which was reinforced from the acquisition of Maxim wound up being the most significant development chauffeur for the automobile sector, which had the greatest development rate out of all sectors (101.5%). Furthermore we formerly recognized “the business just anticipates profits cross-selling chances from 2025 onwards”. Nevertheless, ADI has actually currently begun to take advantage of cross-selling chances as seen from management’s declaration in Q4 2022 profits rundown …

Notably, our style pipeline is starting to take advantage of cross-selling our ADI and Maxim portfolios. This puts us on a course to attain our target $1 billion in profits synergies. For instance, at a European automobile producer, we built on our strong audio connection position to cross-sell our high-speed GMSL innovation (Maxim item), linking their innovative chauffeur systems. — Vincent Roche, CEO

From its most current profits rundown in Q2 2023, the business’s management pointed out the “nonreligious tailwinds sustaining content development continue to drive ADI’s leading battery management and in-cabin connection services” and grew by 40% YoY, hence suggesting its high development momentum being undamaged.

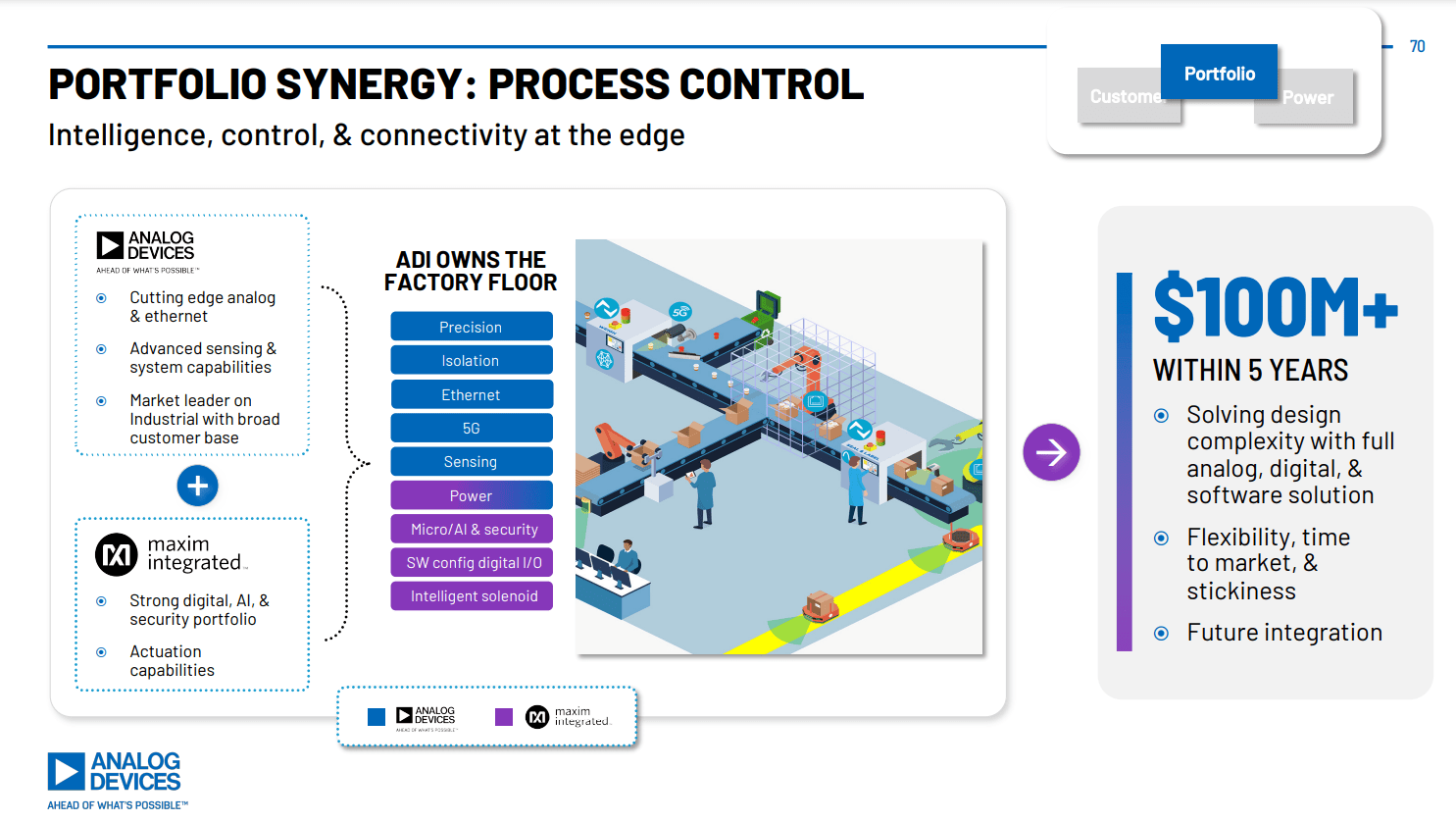

The automobile sector is not the only sector improved by the Maxim acquisition. In its Q2 2022 profits rundown, management mentioned that the interactions sector took advantage of “the innovations that Maxim are giving that wireline location”. ADI likewise took advantage of Maxim’s power and “innovative noticing and system abilities” in the commercial sector, which can be seen in the diagram listed below.

ADI

In regards to success, the business’s gross margin and running margin in 2022 were 64.96% and 31.80% respectively. This is greater than our projections of 63.32% gross margin and 27.69% operating margin. In its Q2 2022 profits rundown, management mentioned that …

The gross margin portion and the development in gross margin portion that you see is actually being driven, as I discussed, by the synergies – Prashanth Mahendra-Rajah, ADI CFO

Furthermore, we recognized “the business anticipated to attain expenses synergies of $275 mln within 24 months after the acquisition”. Nevertheless, in its Q2 2022 profits rundown, management mentioned …

We recorded essentially the whole $275 million that we initially dedicated to as we left our 2nd quarter. Which at Financier Day, we stated we’re raising that target to $400 million, and we’ll strike that number coming out of– or as we leave 2023. That very first $275 million was a bit more slanted towards expense of products, and the following piece will arrange of be well balanced in between expense of products and OpEx. – Prashanth Mahendra-Rajah, ADI CFO

For that reason, the business handled to strike its expense synergy target more than a year previously and increased its target by including $125 mln, which discusses the gross margins and running margins being above our projections.

In conclusion, the bulk (41.7%) of the 64.2% overall business development in 2022 was credited to Maxim Semiconductor, with the staying 22.5% of the development credited to natural ADI development, much greater than our anticipated natural development of 6.64% in our previous protection. We discover that Maxim improved the automobile sector development with its power management systems enhancing ADI’s BMS portfolio, which was the most significant development chauffeur for the automobile sector (101.5% sector development). Furthermore, expense synergies assisted increase ADI’s gross margin (64.96%) and running margin (31.80%), which was greater compared to our projections of 63.32% and 27.69% respectively.

Maxim to Continue Boosting Profits Development

|

New Item Releases |

Overall Business Products |

Maxim Products |

Maxim as a % of Overall Products |

|

December 2022 to Might 2023 |

111 |

47 |

42.3% |

|

June 2022 to December 2022 |

90 |

23 |

25.6% |

Source: ADI, Khaveen Investments

|

Item Applications |

Industrial |

Automotive |

Communications |

Customer |

|

Maxim Products (December 2022 to Might 2023) |

17 |

24 |

5 |

15 |

|

Maxim Products (June 2022 to November 2022) |

12 |

7 |

3 |

5 |

Source: ADI, Khaveen Investments

In the very first table above, we evaluated the brand-new item releases from the entire business and likewise the brand-new items that were from Maxim. In the previous 6 months, the business launched an overall of 111 items, of which 47 of those were Maxim items. In the 6 months prior to that, the business launched an overall of 90 items, and 23 of those were Maxim items. For that reason, the variety of brand-new items from Maxim has more than doubled and Maxim items as a portion of overall business items went from 25.6% in the very first 6 months to 42.3% in the next 6 months. Furthermore, from the 2nd table, the brand-new Maxim items in the previous 6 months have more applications in all 4 sectors (Industrial, Automotive, Communications, and Customer) than the brand-new Maxim items launched 6 months previously.

We formerly anticipated incomes by taking market development projections for each sector, from which we obtained a post-acquisition overall business development projection of 6.7%. Nevertheless, as we recognized in the point above, ADI had natural development of 22.5% in 2022, somewhat greater than analog market development of 20.8%. For that reason, omitting the result of the 41.7% business development from Maxim, the business has actually currently had the ability to grow greater than the marketplace. Hence, with the standard development of the business being much greater than our previous protection, our company believe it is not proper to utilize market CAGR to anticipate profits.

|

Organic Profits Development ($’ 000s) |

2018 |

2019 |

2020 |

2021 |

2022 |

5-Year Typical |

|

Maxim Organic Profits |

2,314,330 |

2,191,390 |

2,354,000 |

2,769,600 |

3,052,184 |

|

|

Development Rate % (YoY) |

-6.7% |

-5.3% |

7.4% |

17.7% |

10.2% |

4.66% |

|

ADI Organic Profits |

6,224,689 |

5,991,065 |

5,603,056 |

6,759,786 |

8,961,769 |

|

|

Development Rate % (YoY) |

18.6% |

-3.8% |

-6.5% |

20.6% |

32.6% |

12.33% |

Source: ADI, Maxim, Khaveen Investments

For our brand-new projections, we took the weighted average of the 5-year typical natural development of Maxim and ADI. We approximated Maxim’s 2021 natural profits by prorating the amount of its Q321 (quarter ending March 2021) and Q421 (quarter ending June 2021) incomes for the staying 6 months of the year. Then, we approximated Maxim’s 2022 natural profits by taking 65% of ADI development in 2022 which was credited to Maxim and included it to our anticipated Maxim 2021 natural profits.

We obtained ADI natural profits in 2021 by deducting overall ADI profits by the $558.5 mln of Maxim profits from the acquisition date (August 2021) till completion of ADI’s (October 2021). We then approximated ADI’s 2022 natural profits by taking 35% of overall business development in 2022 which was credited to ADI’s natural development and included it to ADI’s 2021 natural profits.

We recognized above Maxim items using up a bigger part (42.3%) of overall business item releases in the previous 6 months, compared to 25.6% of overall business item releases in the 6 months prior to that. For that reason, our company believe Maxim will still have the ability to drive increased profits development moving forward. We obtained a weighted typical natural development rate for the combined business as follows:

|

Weighted Average Computation |

Figures |

|

Maxim Weight (%) (‘ a’) |

25.4% |

|

Maxim Organic 5-year Typical Development (%) (‘ b’) |

4.7% |

|

ADI Weight (%) (‘ c’) |

74.6% |

|

ADI Organic 5-year Typical Development (%) (‘d’) |

12.3% |

|

Weighted Average Development Rate |

10.4% |

* Weighted-Average Solution: (a x b) + (c x d)

Source: ADI, Khaveen Investments

Utilizing the formula, we obtained a development projection for the business in 2023 at 10.4%. We likewise keep in mind that the business’s real H1 incomes and Q3 assistance of $3.1 bln from its most current profits rundown represent a development of 9.9%, in line with our projections. Tapering the development projection by one percent over the next 4 years as a conservative quote, our anticipated overall business profits over the next 5 years is displayed in the table listed below:

|

Profits Projection ($’ 000s) |

2023F |

2024F |

2025F |

2026F |

2027F |

|

Overall Profits |

13,260,849 |

14,157,603 |

15,113,735 |

16,133,067 |

17,219,653 |

|

Development Rate % (YoY) |

10.4% |

9.4% |

8.4% |

7.4% |

6.4% |

Source: ADI, Maxim, Khaveen Investments

Threat: Increasing Days Stock Impressive

|

Performance Analysis |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

TTM |

Typical |

|

Stock Turnover |

5.87 x |

2.74 x |

2.44 x |

2.50 x |

2.45 x |

2.07 x |

1.95 x |

1.81 x |

1.53 x |

1.47 x |

1.37 x |

2.48 x |

|

Days Stock Impressive (d A ys) |

62 |

133 |

149 |

146 |

149 |

177 |

187 |

202 |

238 |

248 |

266 |

169 |

Source: ADI, Khaveen Investments

Our company believe among the dangers for the business is its increasing days stock impressive which has actually increased from 62 days in 2013 to 248 days in 2022 and 266 days TTM. This is as the business’s stock turnover ratio reduced from 5.87 x to 1.37 x over the duration. This circumstance might suggest degrading stock management or an accumulation of excess stock due to lower need. In its Q4 2022 rundown formerly, management highlighted that it was preparing to hold more stock “throughout these unsure times” and the business was restoring its “pass away bank” which was lowered “over the last number of years”. In its most current rundown, the business restated its “to hold more ended up products stock versus restocking the channel” which added to greater stock days.

Decision

Khaveen Investments

Looking For Alpha, Khaveen Investments

In summary, our company believe ADI has actually become a joint leader in the analog market together with TI, boasting a considerable market share of 17.2%. This represents an exceptional gain from ADI’s 2021 market share of 12.6%, while TI’s market share decreased from 19% in 2021. ADI’s extraordinary development in 2022 (64.2%) significantly added to its increased market share, surpassing the analog market’s development rate of 20.8%. Maxim played a considerable function in ADI’s development, representing 41.7% of its 2022 development. Maxim’s effect was especially significant in ADI’s automobile sector, driving a considerable 101.5% development in its automobile BMS portfolio.

In addition to Maxim’s contribution, we determined ADI experienced more powerful natural development of 32.6% in 2022, exceeding our previous projection of 6.64%. To identify profits projections, we chose a weighted average of the five-year natural development rates of both Maxim and ADI. This method represent ADI’s greater development compared to the general market and thinks about Maxim’s prospective to even more boost profits development through a greater percentage of item releases in the previous 6 months compared to the preceding duration. Based upon these elements, we obtained a weighted typical development rate of 10.4% for 2023, slowly tapering it down by one percent over the following 4 years.

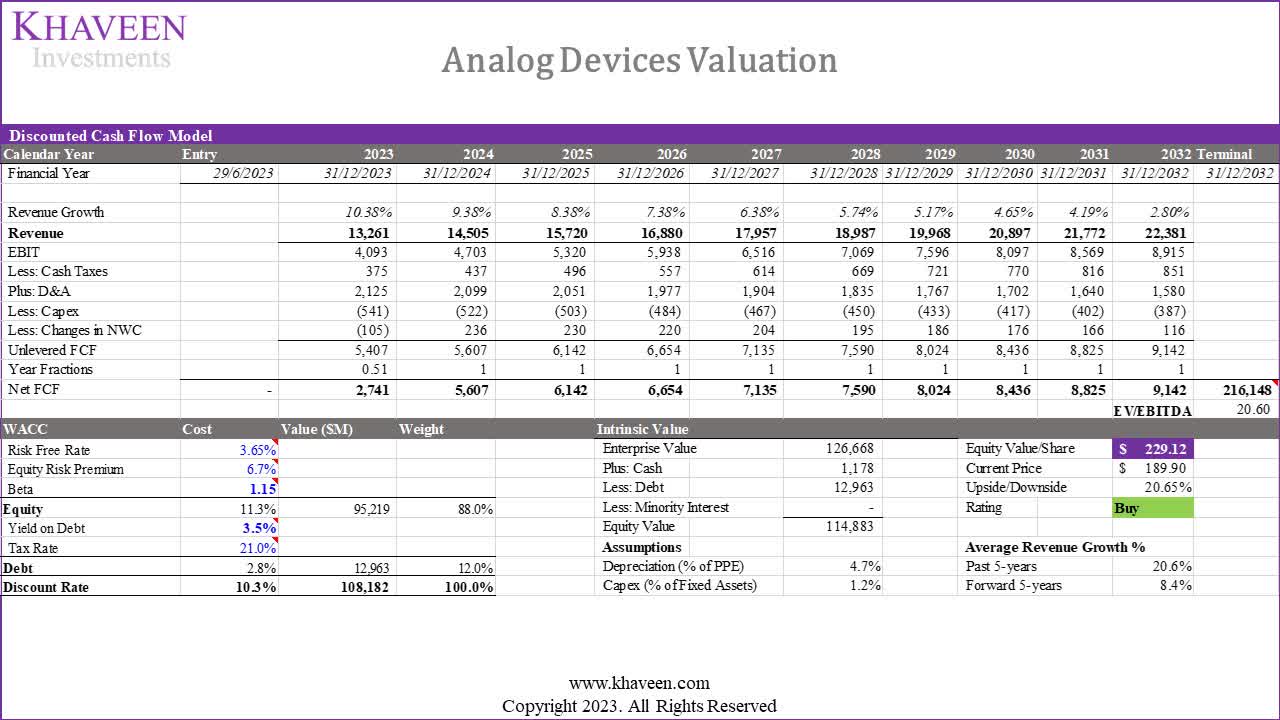

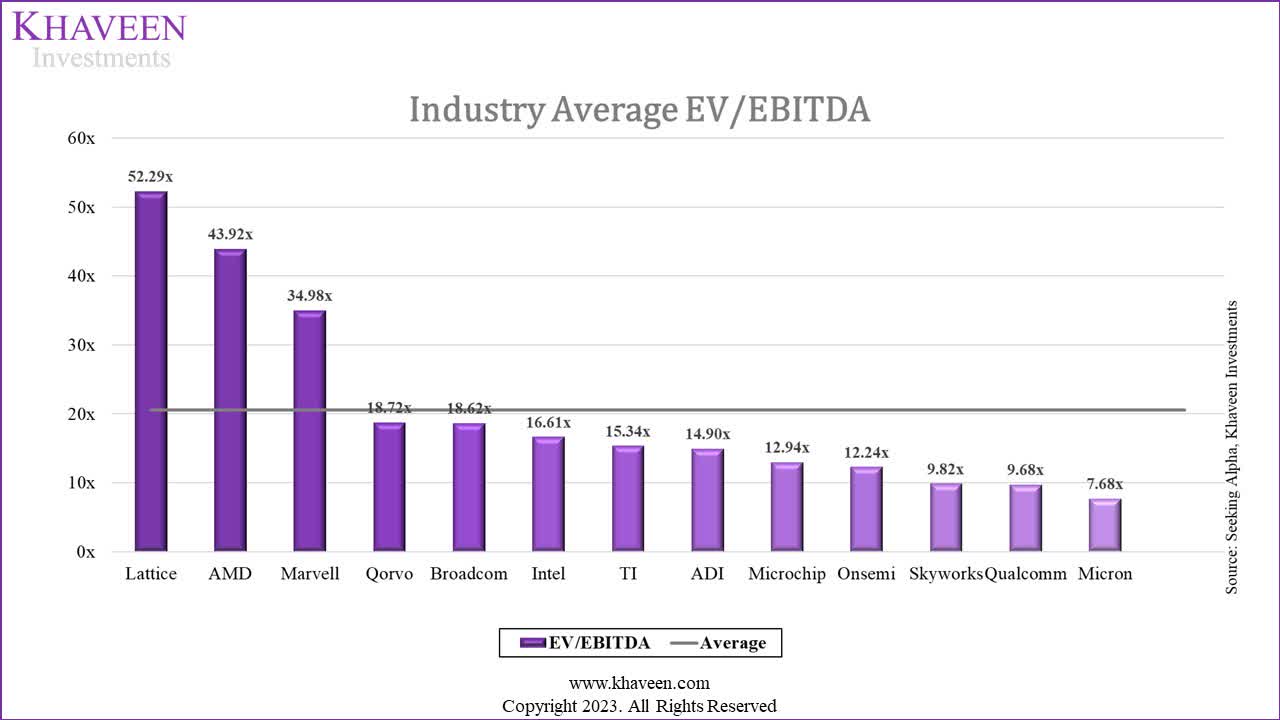

For valuing the business, we used a DCF assessment method. The terminal worth was based upon United States chipmakers’ typical EV/EBITDA ratio, which balanced 20.6 x. We left out Nvidia from this estimation due to its outlier EV/EBITDA ratio of 166.44 x. Significantly, the EV/EBITDA worth we obtained is lower than the one gotten in our previous protection, which stood at 23.87 x.

Subsequently, we got to a cost target of $ 229.12 for ADI, showing an advantage of 20.65%. This brand-new target rate represents a considerable boost of 39% compared to our previous target rate of $164.47. Regardless of the existing stock rate ($ 189.90) exceeding our previous target, our company believe there is still substantial upside prospective. This outlook is driven by our modified projection of an 8.4% forward 5-year development rate (omitting 2022 due to the acquisition), compared to the previous projection of 6.6%. Furthermore, the business’s existing 5-year typical net margin stands at 22.13%, greater than the 20.62% typical net margin from our previous protection and we anticipated greater margins for the business progressing. Taking all these elements into account, we appoint a Buy ranking to Analog Gadgets.