{“page”:0,” year”:2023,” monthnum”:9,” day”:17,” name”:” analyzing-active-in-australia-lessons-from-the-spiva-australia-mid-year-2023-scorecard”,” mistake”:””,” m”:””,” p”:0,” post_parent”:””,” subpost”:””,” subpost_id”:””,” accessory”:””,” attachment_id”:0,” pagename”:””,” page_id”:0,” 2nd”:””,” minute”:””,” hour”:””,” w”:0,” category_name”:””,” tag”:””,” feline”:””,” tag_id”:””,” author”:””,” author_name”:””,” feed”:””,” tb”:””,” paged”:0,” meta_key”:””,” meta_value”:””,” sneak peek”:””,” s”:””,” sentence”:””,” title”:””,” fields”:””,” menu_order”:””,” embed”:””,” classification __ in”: [],” classification __ not_in”: [],” classification __ and”: [],” post __ in”: [],” post __ not_in”: [],” post_name __ in”: [],” tag __ in”: [],” tag __ not_in”: [],” tag __ and”: [],” tag_slug __ in”: [],” tag_slug __ and”: [],” post_parent __ in”: [],” post_parent __ not_in”: [],” author __ in”: [],” author __ not_in”: [],” search_columns”: [],” ignore_sticky_posts”: incorrect,” suppress_filters”: incorrect,” cache_results”: real,” update_post_term_cache”: real,” update_menu_item_cache”: incorrect,” lazy_load_term_meta”: real,” update_post_meta_cache”: real,” post_type”:””,” posts_per_page”:” 5″,” nopaging”: incorrect,” comments_per_page”:” 50″,” no_found_rows”: incorrect,” order”:” DESC”}

[{“display”:”Craig Lazzara”,”title”:”Managing Director, Index Investment Strategy”,”image”:”/wp-content/authors/craig_lazzara-353.jpg”,”url”:”https://www.indexologyblog.com/author/craig_lazzara/”},{“display”:”Tim Edwards”,”title”:”Managing Director, Index Investment Strategy”,”image”:”/wp-content/authors/timothy_edwards-368.jpg”,”url”:”https://www.indexologyblog.com/author/timothy_edwards/”},{“display”:”Hamish Preston”,”title”:”Head of U.S. Equities”,”image”:”/wp-content/authors/hamish_preston-512.jpg”,”url”:”https://www.indexologyblog.com/author/hamish_preston/”},{“display”:”Anu Ganti”,”title”:”Senior Director, Index Investment Strategy”,”image”:”/wp-content/authors/anu_ganti-505.jpg”,”url”:”https://www.indexologyblog.com/author/anu_ganti/”},{“display”:”Fiona Boal”,”title”:”Managing Director, Global Head of Equities”,”image”:”/wp-content/authors/fiona_boal-317.jpg”,”url”:”https://www.indexologyblog.com/author/fiona_boal/”},{“display”:”Jim Wiederhold”,”title”:”Director, Commodities and Real Assets”,”image”:”/wp-content/authors/jim.wiederhold-515.jpg”,”url”:”https://www.indexologyblog.com/author/jim-wiederhold/”},{“display”:”Phillip Brzenk”,”title”:”Managing Director, Global Head of Multi-Asset Indices”,”image”:”/wp-content/authors/phillip_brzenk-325.jpg”,”url”:”https://www.indexologyblog.com/author/phillip_brzenk/”},{“display”:”Howard Silverblatt”,”title”:”Senior Index Analyst, Product Management”,”image”:”/wp-content/authors/howard_silverblatt-197.jpg”,”url”:”https://www.indexologyblog.com/author/howard_silverblatt/”},{“display”:”John Welling”,”title”:”Director, Global Equity Indices”,”image”:”/wp-content/authors/john_welling-246.jpg”,”url”:”https://www.indexologyblog.com/author/john_welling/”},{“display”:”Michael Orzano”,”title”:”Senior Director, Global Equity Indices”,”image”:”/wp-content/authors/Mike.Orzano-231.jpg”,”url”:”https://www.indexologyblog.com/author/mike-orzano/”},{“display”:”Wenli Bill Hao”,”title”:”Senior Lead, Factors and Dividends Indices, Product Management and Development”,”image”:”/wp-content/authors/bill_hao-351.jpg”,”url”:”https://www.indexologyblog.com/author/bill_hao/”},{“display”:”Maria Sanchez”,”title”:”Director, Sustainability Index Product Management, U.S. Equity Indices”,”image”:”/wp-content/authors/maria_sanchez-527.jpg”,”url”:”https://www.indexologyblog.com/author/maria_sanchez/”},{“display”:”Shaun Wurzbach”,”title”:”Managing Director, Head of Commercial Group (North America)”,”image”:”/wp-content/authors/shaun_wurzbach-200.jpg”,”url”:”https://www.indexologyblog.com/author/shaun_wurzbach/”},{“display”:”Silvia Kitchener”,”title”:”Director, Global Equity Indices, Latin America”,”image”:”/wp-content/authors/silvia_kitchener-522.jpg”,”url”:”https://www.indexologyblog.com/author/silvia_kitchener/”},{“display”:”Akash Jain”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/akash_jain-348.jpg”,”url”:”https://www.indexologyblog.com/author/akash_jain/”},{“display”:”Ved Malla”,”title”:”Associate Director, Client Coverage”,”image”:”/wp-content/authors/ved_malla-347.jpg”,”url”:”https://www.indexologyblog.com/author/ved_malla/”},{“display”:”Rupert Watts”,”title”:”Head of Factors and Dividends”,”image”:”/wp-content/authors/rupert_watts-366.jpg”,”url”:”https://www.indexologyblog.com/author/rupert_watts/”},{“display”:”Jason Giordano”,”title”:”Director, Fixed Income, Product Management”,”image”:”/wp-content/authors/jason_giordano-378.jpg”,”url”:”https://www.indexologyblog.com/author/jason_giordano/”},{“display”:”Qing Li”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/qing_li-190.jpg”,”url”:”https://www.indexologyblog.com/author/qing_li/”},{“display”:”Sherifa Issifu”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/sherifa_issifu-518.jpg”,”url”:”https://www.indexologyblog.com/author/sherifa_issifu/”},{“display”:”Brian Luke”,”title”:”Senior Director, Head of Commodities and Real Assets”,”image”:”/wp-content/authors/brian.luke-509.jpg”,”url”:”https://www.indexologyblog.com/author/brian-luke/”},{“display”:”Glenn Doody”,”title”:”Vice President, Product Management, Technology Innovation and Specialty Products”,”image”:”/wp-content/authors/glenn_doody-517.jpg”,”url”:”https://www.indexologyblog.com/author/glenn_doody/”},{“display”:”Priscilla Luk”,”title”:”Managing Director, Global Research & Design, APAC”,”image”:”/wp-content/authors/priscilla_luk-228.jpg”,”url”:”https://www.indexologyblog.com/author/priscilla_luk/”},{“display”:”Liyu Zeng”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/liyu_zeng-252.png”,”url”:”https://www.indexologyblog.com/author/liyu_zeng/”},{“display”:”Sean Freer”,”title”:”Director, Global Equity Indices”,”image”:”/wp-content/authors/sean_freer-490.jpg”,”url”:”https://www.indexologyblog.com/author/sean_freer/”},{“display”:”Barbara Velado”,”title”:”Senior Analyst, Research & Design, Sustainability Indices”,”image”:”/wp-content/authors/barbara_velado-413.jpg”,”url”:”https://www.indexologyblog.com/author/barbara_velado/”},{“display”:”George Valantasis”,”title”:”Associate Director, Strategy Indices”,”image”:”/wp-content/authors/george-valantasis-453.jpg”,”url”:”https://www.indexologyblog.com/author/george-valantasis/”},{“display”:”Cristopher Anguiano”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/cristopher_anguiano-506.jpg”,”url”:”https://www.indexologyblog.com/author/cristopher_anguiano/”},{“display”:”Benedek Vu00f6ru00f6s”,”title”:”Director, Index Investment Strategy”,”image”:”/wp-content/authors/benedek_voros-440.jpg”,”url”:”https://www.indexologyblog.com/author/benedek_voros/”},{“display”:”Michael Mell”,”title”:”Global Head of Custom Indices”,”image”:”/wp-content/authors/michael_mell-362.jpg”,”url”:”https://www.indexologyblog.com/author/michael_mell/”},{“display”:”Maya Beyhan”,”title”:”Senior Director, ESG Specialist, Index Investment Strategy”,”image”:”/wp-content/authors/maya.beyhan-480.jpg”,”url”:”https://www.indexologyblog.com/author/maya-beyhan/”},{“display”:”Andrew Innes”,”title”:”Head of EMEA, Global Research & Design”,”image”:”/wp-content/authors/andrew_innes-189.jpg”,”url”:”https://www.indexologyblog.com/author/andrew_innes/”},{“display”:”Fei Wang”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/fei_wang-443.jpg”,”url”:”https://www.indexologyblog.com/author/fei_wang/”},{“display”:”Rachel Du”,”title”:”Senior Analyst, Global Research & Design”,”image”:”/wp-content/authors/rachel_du-365.jpg”,”url”:”https://www.indexologyblog.com/author/rachel_du/”},{“display”:”Izzy Wang”,”title”:”Analyst, Strategy Indices”,”image”:”/wp-content/authors/izzy.wang-326.jpg”,”url”:”https://www.indexologyblog.com/author/izzy-wang/”},{“display”:”Jason Ye”,”title”:”Director, Factors and Thematics Indices”,”image”:”/wp-content/authors/Jason%20Ye-448.jpg”,”url”:”https://www.indexologyblog.com/author/jason-ye/”},{“display”:”Joseph Nelesen”,”title”:”Senior Director, Index Investment Strategy”,”image”:”/wp-content/authors/joseph_nelesen-452.jpg”,”url”:”https://www.indexologyblog.com/author/joseph_nelesen/”},{“display”:”Jaspreet Duhra”,”title”:”Managing Director, Global Head of Sustainability Indices”,”image”:”/wp-content/authors/jaspreet_duhra-504.jpg”,”url”:”https://www.indexologyblog.com/author/jaspreet_duhra/”},{“display”:”Eduardo Olazabal”,”title”:”Senior Analyst, Global Equity Indices”,”image”:”/wp-content/authors/eduardo_olazabal-451.jpg”,”url”:”https://www.indexologyblog.com/author/eduardo_olazabal/”},{“display”:”Ari Rajendra”,”title”:”Senior Director, Head of Thematic Indices”,”image”:”/wp-content/authors/Ari.Rajendra-524.jpg”,”url”:”https://www.indexologyblog.com/author/ari-rajendra/”},{“display”:”Louis Bellucci”,”title”:”Senior Director, Index Governance”,”image”:”/wp-content/authors/louis_bellucci-377.jpg”,”url”:”https://www.indexologyblog.com/author/louis_bellucci/”},{“display”:”Daniel Perrone”,”title”:”Director and Head of Operations, ESG Indices”,”image”:”/wp-content/authors/daniel_perrone-387.jpg”,”url”:”https://www.indexologyblog.com/author/daniel_perrone/”},{“display”:”Srineel Jalagani”,”title”:”Senior Director, Thematic Indices”,”image”:”/wp-content/authors/srineel_jalagani-446.jpg”,”url”:”https://www.indexologyblog.com/author/srineel_jalagani/”},{“display”:”Raghu Ramachandran”,”title”:”Head of Insurance Asset Channel”,”image”:”/wp-content/authors/raghu_ramachandram-288.jpg”,”url”:”https://www.indexologyblog.com/author/raghu_ramachandram/”},{“display”:”Narottama Bowden”,”title”:”Director, Sustainability Indices Product Management”,”image”:”/wp-content/authors/narottama_bowden-331.jpg”,”url”:”https://www.indexologyblog.com/author/narottama_bowden/”}]

Examining Active in Australia: Lessons from the SPIVA Australia Mid-Year 2023 Scorecard

-

Classifications

Equities, Fixed Earnings -

Tags

2023, active management, Anu Ganti, Australia FA, Australian bonds, Australian equities, set earnings, international equities, S&P Australia Financial Investment Grade Corporate Bond Index, S&P Established Ex-Australia LargeMidCap, S&P/ ASX 200, S&P/ ASX Australian Fixed Interest 0+ Index, SPIVA, SPIVA Australia

Considering That 2013, our SPIVA ®(* )Australia Scorecards have actually revealed that most of actively handled Australian equity funds have actually usually underperformed the S&P/ ASX 200 According to the just recently released SPIVA Australia Mid-Year 2023 Scorecard, 55% of Australian Equity General fund supervisors lagged the S&P/ ASX 200 in the very first half of 2023. Outcomes for some fund classifications were bleaker, with 74% of International Equity General fund supervisors underperforming the

S&P Established Ex-Australia LargeMidCap in the very first half of 2023. We can utilize design predisposition, which plays a significant function in describing active supervisor outperformance, to disentangle this blended set of outcomes. For instance, in our SPIVA report, we discovered that domestic equity supervisors might have gained from direct exposure to abroad markets, which have actually exceeded Australian big caps up until now this year. Nevertheless, design predisposition can be a double-edged sword, as Australian worldwide equity supervisors may have dealt with headwinds from the outperformance of the U.S. relative to other worldwide markets. In Australian dollar terms, the

S&P 500 ®(* )exceeded the S&P Established Ex-U.S. LargeMidCap 1 by 5% over the six-month duration ending in June. This is a moderate degree of relative strength by historic requirements, as we observe in Display 1: 2013, 2014, 2016 and 2021 were years of considerable U.S. outperformance in which, possibly not coincidentally, we likewise reported the greatest worldwide active fund underperformance rates of any SPIVA report, recommending a possible aggregate underweight to U.S. equities relative to the criteria. 2 On The Other Hand, Australian Mutual funds carried out reasonably much better than their large-cap equity equivalents, with a bulk outperformance of 55%. Once again, possibly venturing beyond Australia to get credit direct exposures played a beneficial function. Display 2 shows that active Australian Mutual funds have actually tended to outshine when internationally domiciled or provided Australian dollar-denominated business bonds of comparable credit quality have actually carried out well relative to their in your area provided peers. Since mid-year 2023, the S&P Australia Financial Investment Grade Corporate Bond Index

exceeded the criteria S&P/ ASX Australian Fixed Interest 0+ Index by 1%. Design predispositions been available in lots of types and can assist describe the probability of active outperformance throughout both equities and set earnings markets. Comprehending these predispositions and identifying them from real security choice ability might offer important insights for Australian property owners when making supervisor choice choices. The author wishes to thank Grace Stoddart for her contributions to this post.

1

S&P Established Ex-U.S. LargeMidCap had a 6% weight in Australia since August 31, 2023.

2 S&P Established Ex-Australia LargeMidCap had a 68% weight in the U.S. since August 31, 2023.

The posts on this blog site are viewpoints, not guidance. Please read our Disclaimers

Classifications Equities,

https://www.youtube.com/watch?v=S3g5H_6rOnU

The posts on this blog site are viewpoints, not guidance. Please read our

S&P U.S. Indices Mid-Year 2023: Examining Relative Go Back To CRSP Classifications

Equities

-

Tags

2023, -

Cristopher Anguiano,

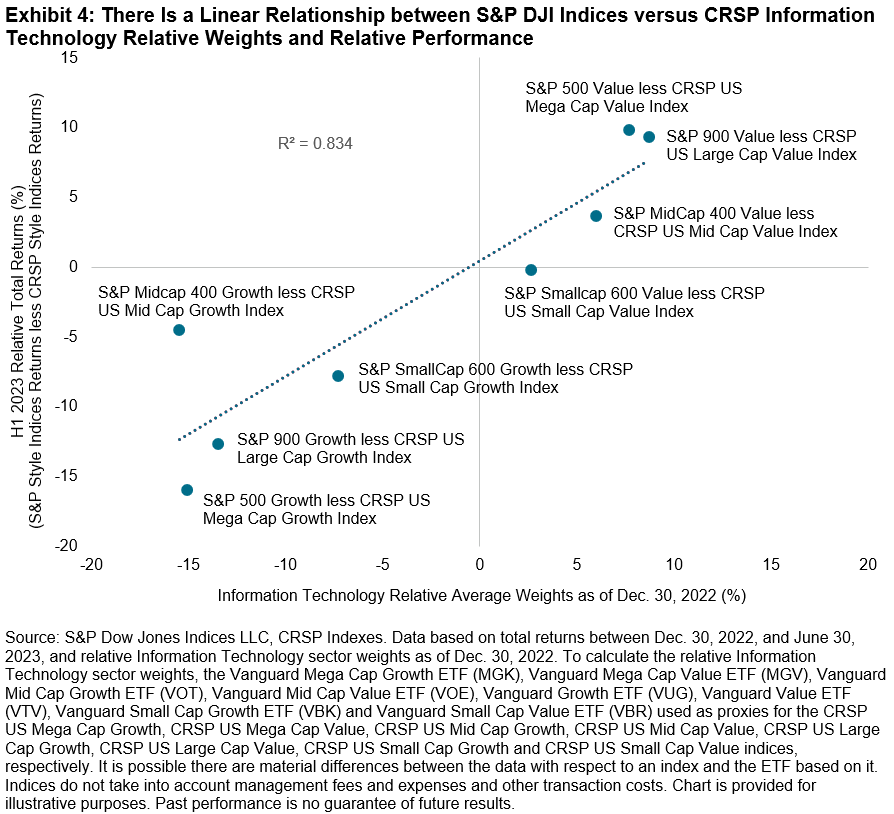

Index Building And Construction, infotech, S&P 1000, S&P 500, S&P 500 Infotech, S&P 500 Leading 50, S&P 900, S&P Composite 1500, S&P MidCap 400, S&P SmallCap 600, S&P U.S. Equity Indices, Design, U.S. Equities, United States FA Following a tough 2022, H1 2023 hosted a healing amongst U.S. equities: the S&P 500 ®

(up 16.9%) published its fourth-best very first half because 1996, and there were gains throughout the marketplace cap spectrum. However on a relative basis, and in contrast to longer horizons, the S&P Core U.S. Equity Indices lagged their CRSP equivalents in H1 2023 (see Display 1). The notified reader understands that 2023 has actually been a strong year for mega caps and Infotech business. Undoubtedly, the S&P 500 Infotech

(42.8%) and S&P 500 Leading 50 (27.6%) published their finest first-half efficiency because 1996 (see Display 2). Considered That S&P DJI’s indices gained from having less direct exposure to Infotech in 2022, one may anticipate this assisted to describe relative efficiency in H1 2023. Display 3 shows that the S&P 500’s relative efficiency in H1 2023 was impeded by its lower weight in Infotech. The Brinson attribution results program that less direct exposure to the Infotech sector contributed adversely to the S&P 500 (-0.6%). Integrated with the unfavorable choice result in Infotech (-0.6%)– the S&P 500 and the CRSP United States Mega Cap Index (as represented by the Lead Mega Cap Index Fund as a proxy) have various constituents owing to distinctions in index building– most likely around 50% of the S&P 500’s underperformance was credited to Infotech. The effects of Infotech weight were a lot more obvious throughout design indices: Display 4 reveals that S&P Design Indices with more (less) direct exposure to Infotech out- (under-) performed their CRSP equivalents in H1 2023. For instance, the

S&P 500 Worth

and S&P 900 Worth published their finest relative H1 returns over the last ten years, beating their CRSP equivalents by 9.9% and 9.3%, respectively. On the other hand, the S&P 500 Development and S&P 900 Development published their worst relative H1 returns over the exact same duration, lagging their CRSP equivalents by 15.9% and 12.6%, respectively. Different CRSP index-based ETFs are utilized as proxies for the CRSP indices listed below. The very first half of 2023 when again highlighted the significance of index building when examining index attributes, provided various direct exposures can assist to describe efficiency distinctions in between indices with comparable sounding goals. The posts on this blog site are viewpoints, not guidance. Please read our

Disclaimers

Tags 2023,

Method

-

Tags

diversity, -

vibrant allowance,

equity futures, Repaired Indexed Annuities, insurance coverage, long treasury futures, multi-asset, danger control, S&P 500 Duo Swift Index, S&P 500 e-mini futures, brief treasury futures, treasury futures How is intraday volatility rebalancing assisting brand-new multi-asset indices quickly react to altering markets? Look inside the S&P 500 Duo Swift Index, a varied, multi-asset, risk-controlled index that is vibrant by style. https://www.youtube.com/watch?v=YEo6_OiP474

The posts on this blog site are viewpoints, not guidance. Please read our

Disclaimers

Tags diversity,

1

Today, our growing need for this resource has actually minimized this protection to less than 40%. Trading of timber-linked items has actually seen huge development in the previous years. 2

This cravings for wood is anticipated to grow a lot more in the coming years. 3 Although domestic need stays the crucial motorist for wood, other usage cases like paper, product packaging, plywood, and so on, assistance need variety for wood. 4 Buying Lumber Lumber is a genuine property and investing in it usually includes ownership of the arrive on which the lumber-producing trees grow. Lumber, being a physical property, supplies your common inflation security part, however, unlike lots of other genuine properties, has the distinct function of biological development throughout times of volatility and depressed need.

5

The alternative of versatile timing of harvests throughout low need can ravel a few of the cost volatility of wood financial investments. Price quotes put almost 60% of the forestlands in the U.S. as independently owned. 6 Capital allowance to lumber producing forestlands has actually typically been within the world of big institutional financiers that straight own the forestlands and can utilize intermediaries (e.g., Forest Financial investment Management Organizations ) to handle these lands. Know-how in forestry and land management, integrated with reasonably long hold-up durations and illiquidity, have actually been leading chauffeurs for active management of these properties. Nevertheless, Forest REITs bring the exact same knowledge in management of forests and are openly traded, supplying relative liquidity, real-time prices and openness for these long-dated properties. In addition, ETFs likewise offer another opportunity of access to wood and associated financial investments through openly traded instruments.

The push towards sustainability as a financial investment objective includes another measurement to wood’s worth in a varied portfolio. Effective water/soil/resource management, ecosystem/biodiversity conservation and favorable environment effect all add to beneficial ecological and sustainability goals. Forests function as a carbon sequestration system, and when wood from these forests is utilized in building, this can even more minimize GHG emissions.[TIMOs] 7

Indexing Technique to Timber-Related Investments The

S&P Global Lumber and Forestry (GTF) Index

, released in 2007, targets direct exposure to timber-related financial investments through public equity stocks throughout industrialized market listings and regional listings from 3 emerging market nations (Brazil, South Korea and South Africa). S&P GTF Index constituents cover the worth chain of the wood environment. To catch a broad investable stock group with thematic significance, the beginning universe of stocks consists of companies from Lumber REITS under the GICS ®

category, 8 together with companies whose earnings originates from sectors appropriate to the forestry service (utilizing the FactSet Revere Service Market Category System). A direct exposure rating structure is used over this group of stocks to keep the index’s thematic pureness. Companies with greater direct exposure ratings are normally viewed as being closer to the core of the wood producing and processing environment. Lumber REITs and Lumber Home Management stocks are provided a greater direct exposure rating, together with pulp mills that can be vertically incorporated, when compared to Paper Mills and Product packaging Products associated business that are more downstream. The index constituents’ weights are based upon each stock’s direct exposure rating and its float market capitalization, based on suitable restraints to prevent concentration danger. In addition, the index approach omits business that are participated in specific service activities (e.g., questionable weapons, tobacco items, and so on) and business that are non-compliant with the United Nations Global Compact (UNGC) standards, and it evaluates business for any reputational danger issues.

Since Aug. 30, 2023, the index includes 30 stocks, with 43% weight designated to 11 pure-play business, 16% weight in Lumber REITs stocks and 27% weight to the business with a direct exposure rating of 1.

The index is slanted (56%) towards mid-cap stocks (see Display 2), with the bulk (over 40%) of the direct exposure originating from North American entities, followed by European companies (33%).

1

2 https://www.worldwildlife.org/industries/timber

4 https://caia.org/blog/2023/02/25/exploring-link-between-lumber-prices-and-timber-markets

5 https://www.ipe.com/inflation-assets-timber/37666.article

6 https://cdnsciencepub.com/doi/10.1139/cjfr-2021-0085

7 https://www.fs.usda.gov/research/treesearch/63853

8 For more details please see the

S&P Thematic Indices Method The posts on this blog site are viewpoints, not guidance. Please read our Disclaimers