Vladimir_Timofeev/ iStock through Getty Images

Ceragon Networks Ltd ( NASDAQ: CRNT) has actually sculpted a specific niche in cordless backhaul options, a sector that ought to gain from the development of 5G. In my view, this positions CRNT’s varied offerings, from voice services to IoT connection, to make money from nonreligious tailwinds. CRNT’s current monetary information suggests an appealing margin enhancement. Furthermore, information from their newest incomes call recommend they are preparing for brand-new item launches, lining up with the expected international cordless backhaul market development. Nevertheless, the more comprehensive telecom market has difficulties, particularly with combination. I think CRNT’s fairly modest size may challenge browsing this landscape. In general, based upon my assessment analysis, CRNT’s reasonable worth is around $161.3 million. Provided this evaluation, I believe that its existing market assessment does not provide an especially attracting financial investment proposal, leading me to keep a neutral position on CRNT.

Company Introduction

Ceragon Networks runs in the Innovation and Communications market, with a specific niche in cordless backhaul options. These options are developed to help cellular operators and different provider in boosting their networks, particularly as we shift into the 5G period. The business’s portfolio consists of voice, Machine-to-Machine (M2M) options, broadband, and IoT connection. Provided the quick digital improvement, such offerings are ending up being progressively important. Remarkably, CRNT’s reach isn’t restricted to simply telecoms; they likewise serve public security and overseas drilling sectors. With operations from Asia-Pacific to the Americas and headquartered in Rosh Ha’Ayin, Israel, I think CRNT’s international existence enables them to deal with a broad spectrum of market needs, placing them for possible development in the progressing tech landscape.

In Between December 2022 and June 2023, the business experienced a subtle yet notable development in its overall possessions, increasing from $289.3 M to $294.5 M. This increment, albeit modest, provides a buffer versus unforeseeable market shifts. An essential element of the business’s current monetary trajectory is the exceptional healing in earnings, which transitioned from a $3.8 M loss to a $4.1 M revenue in a simple 6 months. This upward shift, emphasized by a small increase in overall existing possessions from $210.7 M to $215.8 M, suggests boosted functional effectiveness. It’s possible that these effectiveness come from well-executed cost-reduction techniques (more on this later). Likewise, CRNT’s capital characteristics prove this favorable pattern, with net money from running activities transitioning from a $4.9 M deficit to a $6.7 M surplus.

CRNT’s site.

Outlook and Promising Margin Growth

Throughout CRNT’s most current incomes call, the business discussed its approaching item roadmap, highlighting its method to minimize BOM expenses utilizing ASIC developments as 2024 methods. Doron Arazi, the CEO of CRNT, highlighted the business’s commitment to presenting a revamped variation of choose items. These developments are developed to expertly combine technological requirements with factors to consider of overall expense of ownership (TCO). In my view, Arazi’s verification that these items are set for an industrial launching soon enhances the business’s existing offerings and signals a proactive technique to market needs. CRNT’s CEO likewise hinted that a next-generation chip with exceptional capability functions is set up for a 2024 launch. While Arazi prepares for that the profits contribution from this chip may be restricted in its launching year, I think CRNT’s competitive expense structure from the start is motivating. This places the item positively in the market, and as sales volumes increase, there’s capacity for even much healthier gross margins.

Maximize Marketing research (maximizemarketresearch.com)

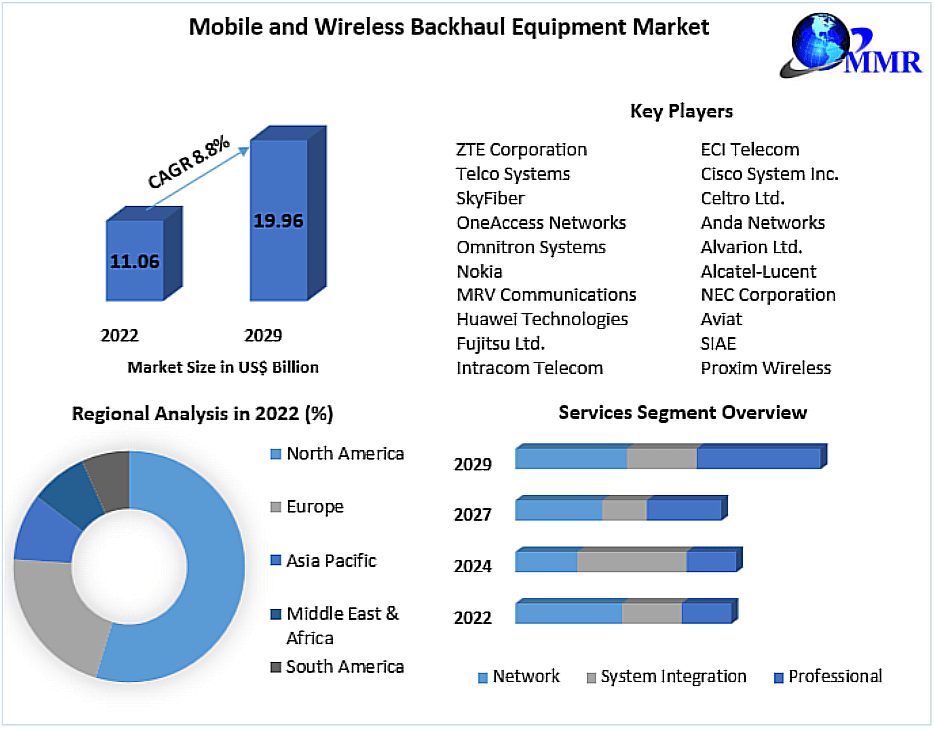

Additionally, thinking about more comprehensive market patterns, the international cordless backhaul market reveals favorable momentum Elements such as the rise in smart device adoption, the rollout of 5G innovation, and the increase in online media usage drive this development These advancements highlight an increasing need for effective information transport options. In my view, the information highlights the marketplace’s appealing capacity. It is expected to grow at a 12.5% CAGR from 2023 to 2028, with forecasts showing a market assessment of around $71.77 billion by 2028. I think that this development trajectory lines up with CRNT’s method to gain from this growing market.

CRNT’s site.

Regrettably, the telecom sector is going through a significant improvement, identified by a clear pattern towards combination. Noteworthy mergers, such as the union of T-Mobile ( TMUS) and Sprint ( S) in the U.S., emphasize this shift. This case provides possible difficulties for business like CRNT. For example, a considerable issue is the possible loss of sales to longstanding clients, particularly when they combine with business that prefer rival items or have existing facilities that negate the requirement for additional services. This unpredictability can stop briefly brand-new collaborations or item orders, affecting profits and development strategies. Additionally, there’s an increasing pattern towards network-sharing contracts, where operators integrate their facilities resources. While this might be economically advantageous for operators, it lowers the need for network devices, possibly affecting profits for companies in this sector.

Assessment Analysis

In my view, we should depend on assessment multiples to examine CRNT’s assessment, because it’s unprofitable For this, I think that provided the business’s service design, it’s affordable to concentrate on the EV/Sales and EV/EBITDA metrics, which are typically utilized for business in the Innovation sector. CRNT’s forward EV/Sales several stands at 0.59, substantially lower by around 77.59% compared to the sector average of 2.63. This scenario recommends that the marketplace worths CRNT’s sales at a discount rate relative to its peers. Furthermore, the forward EV/EBITDA several for CRNT is 6.22, which is likewise substantially lower by about 54.75% than the sector average of 13.76.

CRNT’s monetary discipline appears in its handling of operating costs The business has actually kept its R&D expenses at $7.6 million, representing 8.8% of profits, below 10.6% in the previous year. This shift indicates that CRNT is attaining more with its R&D financial investments. Furthermore, sales and marketing expenditures have actually been structured to $9.4 million or 10.9% of profits, a decline from the previous year’s 12.8%. Nevertheless, a minor uptick in General and Administrative expenditures from 6.5% to 7.0% recommends the requirement for ongoing oversight.

Looking for Alpha plus author’s elaboration.

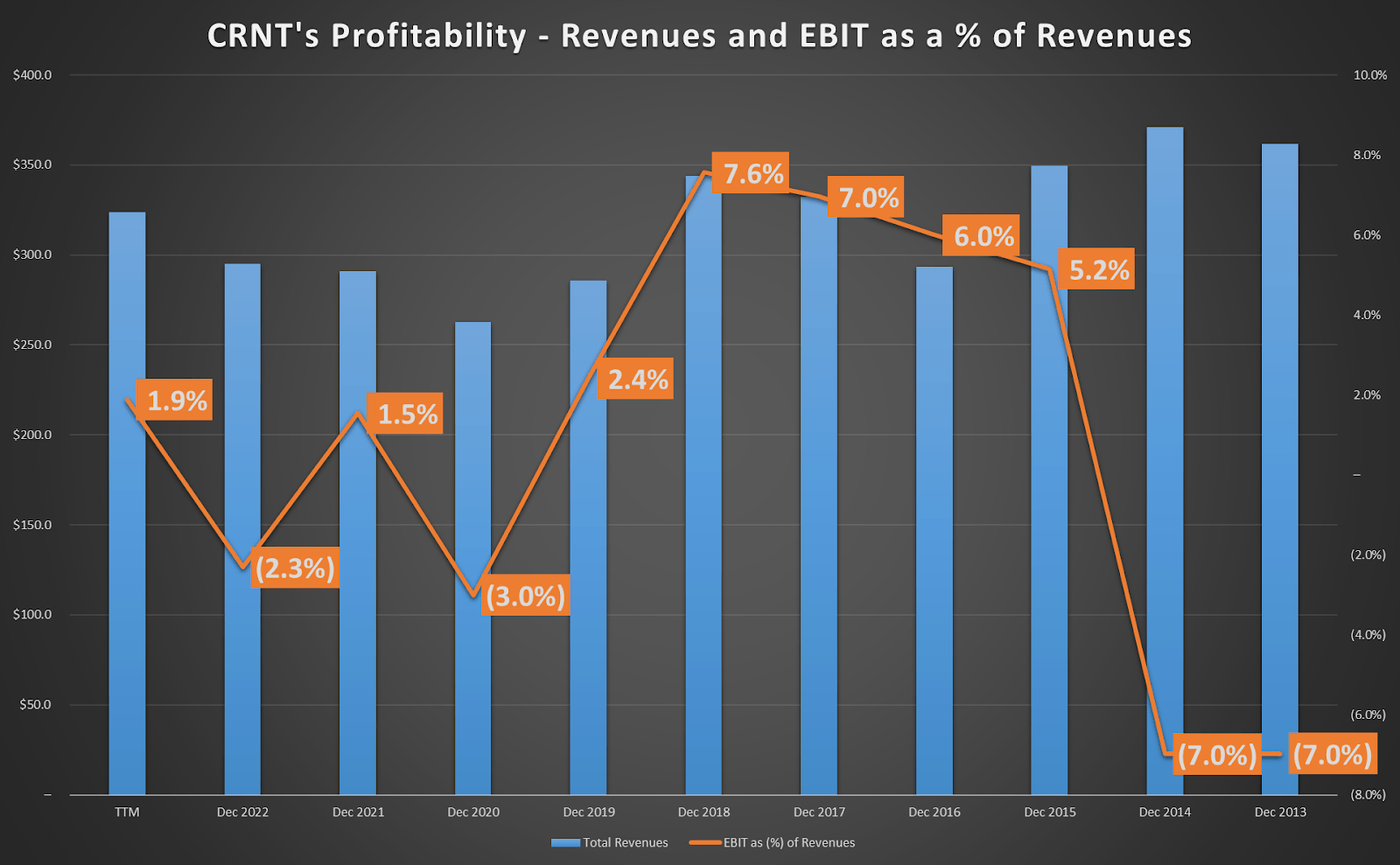

I think CRNT’s forward-thinking technique is highlighted by its anticipated operating costs, which vary in between $22 million and $23 million for the 2nd half of 2023. This would lead to an annualized figure of as much as $92 million, marking an enhancement from the average of $95.9 million because 2013. For context, CRNT’s EBIT margins have actually hovered around 1.1% because 2013, with a current uptick to 1.9% in the TTM, recommending a favorable trajectory affected by functional improvements. The preliminary indications of margin growth and a reputable CAGR of 6.0% in profits because 2020 recommend CRNT is close to attaining success.

TradingView.

Provided its continuous margin enhancements, I believe it’s affordable for CRNT’s EBIT margin to support at 2.5% of yearly run rate profits of $350 million. For this reason, thinking about the sector’s average EV/EBIT ratio of around 18, I obtain a yearly EBIT run rate of $8.75 million. Utilizing a conservative EV/EBIT multiple of 15, CRNT’s business worth is approximated at $131.3 million. After representing money and financial obligation modifications, the suggested reasonable worth is $161.3 million. Therefore, CRNT appears relatively priced compared to its market capitalization of $170 million. While CRNT displays appealing service basics, its existing stock assessment does not provide an engaging buy chance, leading me to provide it a neutral score.

Conclusions

Total, CRNT deals a varied portfolio that appears appropriate to satisfy the needs of a significantly digital world. The business’s current monetary turning points and forward-thinking item efforts recommend the capacity for margin enhancement. Plus, I think the anticipated development of the international cordless backhaul market highlights these chances. Nevertheless, the continuous pattern of combination in the telecom sector provides difficulties. And, provided CRNT’s existing absence of success, these difficulties necessitate cautious factor to consider. Therefore, based upon my appraisal evaluation, CRNT seems trading near its intrinsic worth, leading me to keep a neutral position on the stock. The factor for this is the balance in between the business’s development potential customers and the intrinsic threats in the sector.