SOPA Images/LightRocket through Getty Images![]()

An exceptional organization design

Pagaya Technologies ( NASDAQ: PGY) is a good story with possible unbalanced returns offered the exceptionally low evaluation of $1.11 and a market cap of simply $855Mn. Pagaya is a Fintech, choice and shovels, AI play supplying a platform/software service to industrial lending institutions like Visa, banks, and even Fintech rival SoFi Technologies ( SOFI).

Let’s take a much deeper dive into Pagaya’s organization design. Unlike Upstart, ( UPST) and SoFi Technologies, Pagaya does not keep any loans on its books, other than a little portion of securitizations made by them for obligatory danger retention compliance.

Its organization design is to charges costs to organization customers (lending institutions) like Visa ( V), Ally Financial ( ALLY) and SoFi Technologies to offer due diligence and credit analysis of their prospective debtors – sort through their initially-declined loan applications, and discover any excellent loans amongst the decreased ones.

Pagaya packages these loans and moves them to their last location – financiers. 80% of the loans get bundled into ABS, (Property Backed Securities), which institutional customers have actually consented to buy beforehand. The other 20% of the bundled loans are offered to personal financiers, and Pagaya charges them a cost for that service

Pagaya gets costs from 3 sources.

- Platform and licensing costs, from providing partners for utilizing Pagaya’s’s AI service.

- ABS bundling costs – These are markups made by Pagaya before they are taken into ABS structures, plus other costs for product packaging the ABS.

- Loan or Financier Costs – These are credited the other financiers who do not purchase ABS, rather they purchase the loans straight for their books.

Pagaya’s Company Design ( Pagaya)

The Bull Case

How do I anticipate this organization to flourish? Besides its own advantages this design supplies advantages for the other 2 celebrations too, customer dealing with lending institutions and the ABS purchasers or financiers.

Financier advantages:

- ABS– Property Backed Securities of vehicle loans, individual loans or PoS (Point of Sale– Buy Now Pay Later) make a lot more than treasuries. 8-12% according to Bert

- The buyers/investors’ danger is expanded throughout various sectors (vehicle, home, and individual) and throughout various lending institutions.

- Given That Pagaya is the greatest company of customer ABS’, big organizations get enough liquidity to make it worth the effort.

Pagaya is the among the marketplace leaders in the ABS market, and the # 1 in individual loans and clients restore since of big volume offers.

Despite The Fact That they are the biggest companies of individual loan ABS, their ABS’ tend to get oversubscribed, suggesting ongoing need.

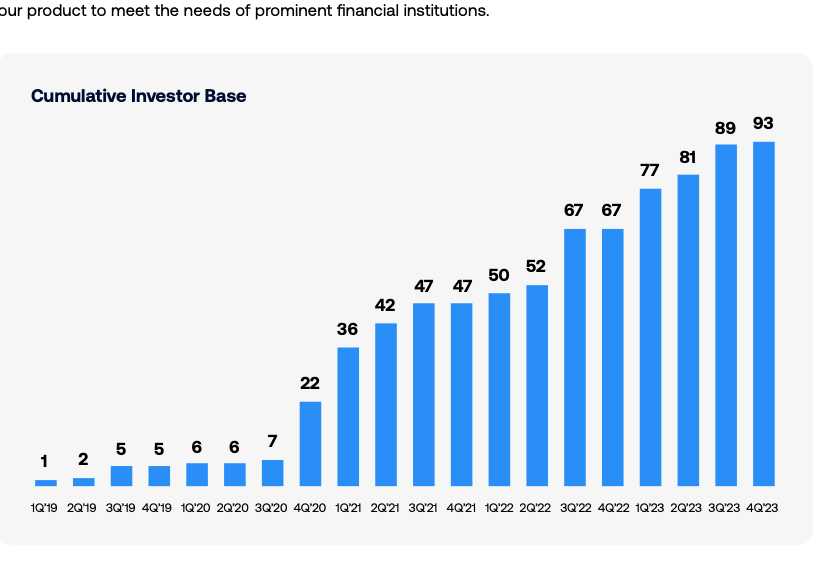

Strong capital and institutional Support – The Singapore Federal Government Fund, which owns 9% of Pagaya is likewise a big purchaser of ABS.

As we see below, the financier base for ABS has actually grown from 1 to 93 in the last 5 years.

Pagaya financier base ( Pagaya)

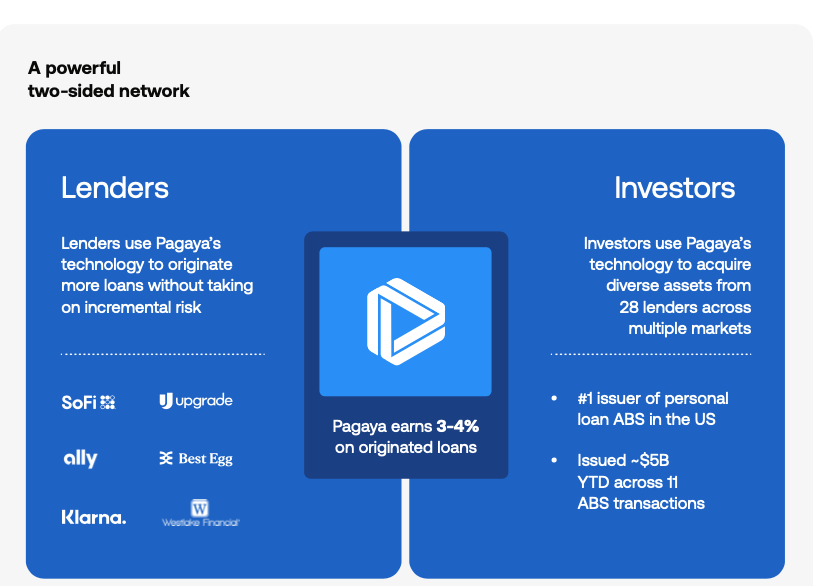

Lending institution advantages:

- The lending institution keeps the debtor as a client– Pagaya is the lending institution’s due diligence/credit evaluation/ expert system arm.

- Lenders take no balance sheet danger– loans are instantly bundled as ABS.

- Lenders get most of in advance costs, providing a little part to Pagaya.

Strong customer base – Pagaya has an outstanding list of lending institutions it works with as we can see from the chart above – Ally Financial, SoFi Technologies, Finest Egg and Klarna. It likewise has the leviathan Visa, Upgrade, Prosper and got Westlake Financial, a car lending institution with $24Bn in properties in September 2023, providing it access to Westlake’s 14,000 franchise dealers.

Smooth Experience – Pagaya has strong relationships with lending institutions since of the smooth experience. The debtor does not even understand that they are handling Pagaya. As an outcome, lending institutions likewise do not fear them since they’re not thinking about getting their customers– they’re not because organization and are a pure service play.

This is a repeating, sustainable organization satisfying a requirement— anybody in the financing organization or credit organization requires it to secure from credit losses. Cherry selecting loans utilizing much better intelligence with more information points assists accomplish standard or much better returns for its providing partners.

AI provides an one-upmanship – While presently it is a strong AI/ Artificial intelligence have fun with Pagaya offering a number of information points for analysis, I do wish to stress that credit appraisals and diligence has actually been around permanently, however offered Pagaya’s prevalent adoption, an AI platform for credit appraisals is most likely to end up being a market requirement or requirement.

Scale – Besides the AI differentiator, I think the other significant strength is scale with ABS purchasers and lending institution relationships.

No credit danger *— Pagaya’s ABS offers are pre-funded, Pagaya needs to discover credit worthwhile debtors rather of aiming to unload bad loans.

*( Like all securitization companies, Pagaya needs to maintain 5% of its securitizations to preserve danger retention compliance with federal government guidelines.)

No customer acquisition expenses— lending institutions spend for that.

Changing Expenses— It takes Pagaya and the lending institution about 2-3 years to total onboarding and combination.

A tighter credit environment – the existing post Silicon Valley crisis environment in the middle of brand-new guidelines and oversight motivates lending institutions to de-risk, which suggests keeping less loans on their books and more securitization resulting in higher need for Pagaya. This is a tailwind and not an obstacle.

From CEO, Gal Krubiner on the Q3-23 revenues call, focus mine

Yes, so let me begin with the lending institutions and after that Mike will take the financier side. From the lending institution side, there is once again, another really strong tailwind to our item all the item, that the truth that our banks are aiming to provide the option to the clients however at the exact same time, have restrictions on the balance sheets, both from liquidity and policy viewpoint. So that drives a great deal of interest in our item, we are concentrating on huge banks and huge vehicle company, which part of our vehicle hostages, which is an open and market that we opened simply recently.

The Bear Case

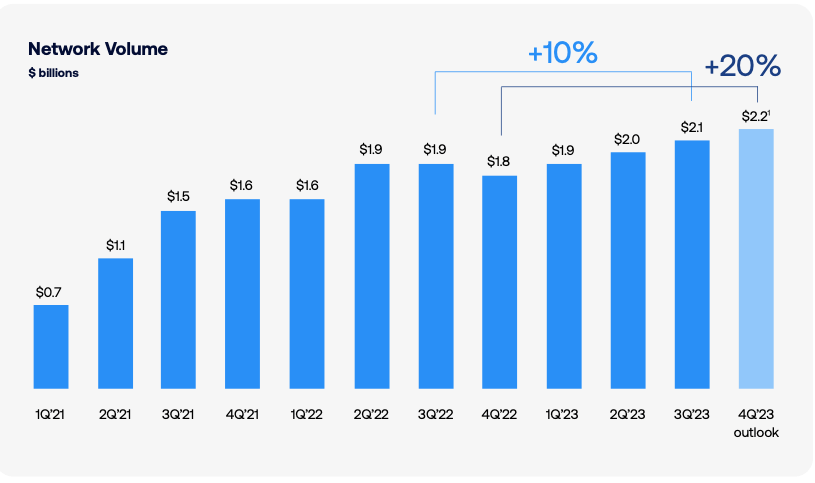

The dreadful 3C – This is a Cutthroat, Product, Cyclical organization and sure there is the AI item differentiator, however with time, even M/L or AI platforms or software application will end up being a commoditized organization, without substantial competitive benefits. While Pagaya does not take credit danger, their organization design depends upon financial conditions and cycles, and the credit value of individual loan and vehicle debtors. If default rates increase, and credit conditions intensify, this will certainly reduce order circulation and volumes. As we see from the network chart in the 2023 area listed below – Network volume flatlined in Q1-2022, at 1.6 Bn, then stagnated at $1.9 Bn in 2 quarters of 2022, with even one reduction to $1.8 Bn. We lastly saw development restoring in Q1-2023 to $1.9 Bn.

Barriers to entry are low— for instance, their lending institution clients might quickly establish the exact same software application. Their lending institutions who are much larger, SoFi Technologies itself is $7.5 Bn in market cap, a little less than 10 times Pagaya’s size,– might become their greatest rivals by purchasing comparable AI software application on their own, get rid of Pagaya and shop their own item around like AWS. Nevertheless, this might be alleviated since of the worth of the information that Pagaya currently has and the hesitation of other lending institutions to share their information with a contending SoFi Technologies, plus there is the worry of guidelines too.

Double capital structure – Pagaya has a double capital structure with higher ballot rights for the co-founders, which is constantly a dangling risk. Based on their last 20F filing, creators held 77% of ballot rights.

Dilution – Another obstacle is the possibility of ongoing dilution. Share count stood at 738Mn shares in Sep 2023 compared to 667Mn in Sep 2022, a boost of 11% …

” Diworsification” danger – Pagaya might constantly raise capital for acquisitions to goose development, or even worse like Upstart keep loans on their books! There is a rack filing for an extra $500 Mn since Oct 2023, which might not be needed and dilutive. Though that appears to be a really not likely situation in the meantime. After seeing Upstart plunge from its peak cost of $311 or Pagaya from $23, I can not think of any management wishing to go through that headache once again.

Non-USA business – Israeli listing, 20-F (for foreign business) reporting requirements are not as stiff as SEC’s 10K’s. This will be alleviated as Pagaya is filing for a United States listing in 2024 and anticipates to offer Q1-2024 according to GAAP, according to this press release on its site. This is a voluntary tactical relocation by Pagaya, to concentrate on enhancing responsibility to investors by supplying quarterly outcomes under GAAP requirements, which will likewise boost openness of its organization, and offer benchmarking and consistency with other United States business. It is likewise moving its head office to New york city City.

Prepayments – While lower rate of interest increase need for all kinds of loanings and for that reason more volumes and sales, there is a disadvantage. As Treasury rates fall, there are a great deal of prepayments, which lowers the worth of the ABS– An ABS’ worth is stemmed from the anticipated interest earnings streams, if the debtor prepays the predicted earnings stream gets lowered.

Monetary business are pariahs – After the Great Financial Crisis, 2023’s SVB and First Republic Crisis, and the existing New york city Neighborhood Bancorp chaos, this sector has actually ended up being a stepchild. Besides, the consistent drumbeat of a possible industrial property crisis resounds throughout the whole financing market.

The Darwin Residences venture – Pagaya gotten Darwin Residences to make lease earnings from Single Household Leasings and there is inadequate exposure on their efficiency yet. Management mentioned that efficiency wasn’t product from this department in their last revenues call. I hope this is not a “Diworsification” as Peter Lynch would have called it.

2023 – Improving metrics all around.

From the chart below, Pagaya started development once again in Q1-2023 and has actually grown network volume progressively to $2.2 Bn.

Pagaya Network Volume ( Pagaya)

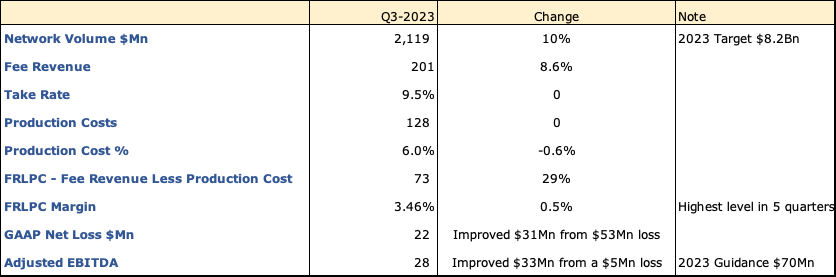

And the increased network volume has actually led to a number of much better metrics as revealed listed below.

Pagaya Metrics ( Pagaya, Looking For Alpha, Fountainhead)

Even as the take rate remained consistent at 9.5%, the charge earnings increased 8.6%, the production expense portion enhanced by 0.6%.

The greatest gainer was the FRLPC, (Cost Earnings Less Production Expense) growing 29% to $73Mn with a 50-basis point enhancement in margins to 3.46% – which was the greatest level in 5 years.

All of this caused Pagaya making $28Mn of adjusted EBITDA in Q3-2023, the very first quarter of a yearly $100Mn adjusted EBITDA run rate. With repaired expenses dropping and margins enhancing, running leveraged has actually placed Pagaya for adjusted EBITDA development in 2024.

From the CFO, Michael Kurlander on the Q3-2023 Revenues Call, focus mine.

Carrying on to running costs, overall core OpEx omitting stock based settlement devaluation and one-time costs has actually now decreased for 4 straight quarters to $52 million, representing a record low of 25% of our overall earnings. Our decrease in costs this year has actually been broad throughout both settlement and non-compensation line products. And we have actually now exceeded the $50 million in run rate cost savings we have actually revealed in our Q1 call. This remains in the context of providing record volumes and profits this quarter, showing the intrinsic operating utilize in our organization, which we prepare for can continue even with the big brand-new partners just recently revealed.

Q4-2023 and Complete Year 2023 Revenues

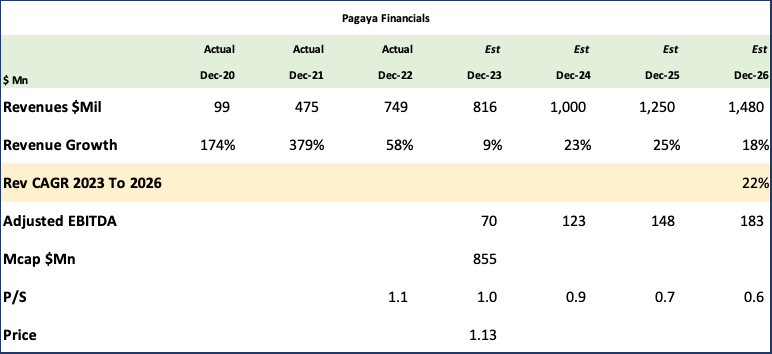

Pagaya reports Q4-2023, and complete year 2023, revenues on February 21, 2024. It has assisted to complete year 2023 changed EBITDA to be at the high-end of the series of $65 to $75Mn and it anticipates complete year network volume to surpass the high-end of its formerly assisted $8Bn to $8.2 B, and earnings to be in line with forecasts of $800 to $825Mn. Experts agreement price quotes according to Looking For Alpha are for profits of $222Mn in Q4, a 15% YoY boost and $816Mn for the complete year, a 9% development. Pagaya continues to succeed.

An Unbalanced Return

I own Pagaya and strategy to keep building up; in my viewpoint the drawback is shown in the cost of $1.12, however the advantage might be a 4 bagger in 5 years. That’s a yearly return of 32%.

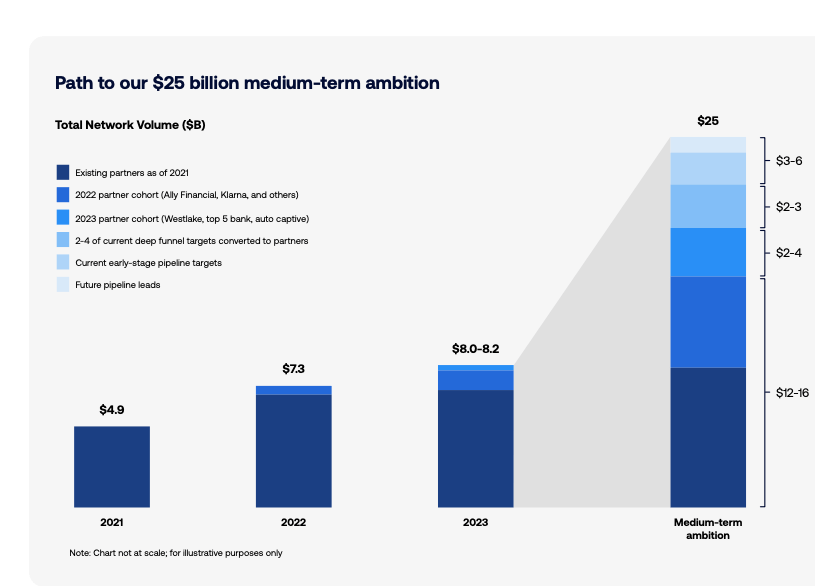

Pagaya definitely has the development to arrive. They increased network volume from $4.9 Bn to an approximated $8.1 Bn in 2 years – a CAGR of 29%. If they take 5 years to accomplish $25Bn in network volume, that’s a CAGR of 25%

They require to include 3 huge lending institutions each year and they have the pipeline to do so. They’re speaking with 80% of the leading 25 banks in various phases and wish to transform 10 handle the next year approximately, as we can see from the beautiful robust pipeline listed below.

Pagaya Pipeline and Network Volume ( Pagaya)

More notably, their organization design assists them in spades, since getting brand-new customers causes onboarding at all its branches and all its items. First year’s earnings is truly simply one piece of the pie, years 2 and 3 total the anticipated development from a brand-new customer as the rollout and combination procedure gets finished. And after that onwards there is sustainable repeating earnings from the exact same customer.

They currently have a $100Mn run rate of adjusted EBITDA of $28Mn from Q3-2023 and based upon my and Looking for Alpha agreement approximates listed below they definitely have the operating utilize to continue growing adjusted EBITA. Management wishes to accomplish $500Mn EBITDA in the medium term and my quote of adjusted EBITDA of $183Mn by Dec 2026, is most likely conservative.

Pagaya Earnings and EBITDA ( Pagaya, Looking For Alpha, Fountainhead)

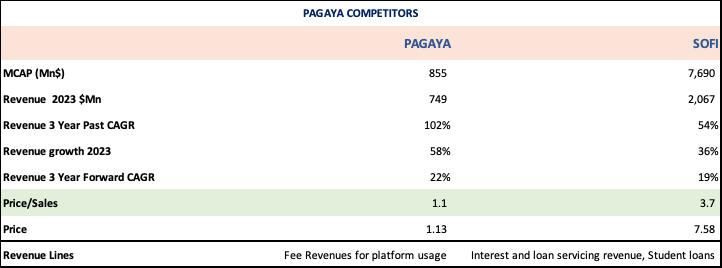

The stock is priced at just 1.05 times sales and with an approximated Sales CAGR of 22%, this drops to 0.6 x sales – it had existing properties of $419Mn in Sep 2023- that’s half its market cap! That’s a take! Compare that to SoFi, which is priced at 3.7 X sales and has a 3 year forward CAGR of 19% lower than Pagaya. Plus, SoFi makes just a part of its profits from services, they make interest earnings too, which brings credit danger.

Pagaya rival ( Pagaya, Looking For Alpha, Fountainhead)

Pagaya is a surprise gem – few experts cover this stock.

They have

- Strong organizations like the Singapore Sovereign Wealth Fund backing them.

- Incredible scale and reach with financiers and lending institutions.

- A big and really trustworthy pipeline.

- A distinct organization design, which de-risks the financing organization in genuine time.

- A platform that works throughout a number of items and lending institutions.

- Anticipated earnings development of 22%.

- Improving margins.

- They will quickly be noted in the United States – that itself might be a substantial increase.

- And can likewise gain from a reverse stock split, which eliminates the more affordable branding of a $1 stock.

What’s not to like?