There was widespread speculation after the Federal Free Market Committee (FOMC) conference recently about the timing and variety of rate of interest cuts this year. In a follow-up interview on 60 Minutes on Sunday, Federal Reserve Chairman Jerome Powell did not seem like somebody who has actually rotated.

In truth, Powell thinks the Fed can wait till it sees more labor damage before cutting the Federal Funds Rate strongly or approaching a neutral policy position, reiterating that a March rate cut is “not likely.”

In December, the Fed spoke about 3 rate cuts in 2024 however some individuals made a case for 4, 5 or perhaps 6 rate cuts provided a Fed pivot. Nevertheless, for me it’s constantly had to do with the labor market and out of work claims information, which information line hasn’t broken enough for the Fed to be more aggressive. For the Fed to cut rates in March, we would require weaker labor information, no matter how low inflation enters the next report.

Here’s part of the interview on 60 Minutes that highlights what I’m speaking about:

Scott Pelley: However inflation has actually been falling progressively for 11 months. You have actually prevented an economic downturn. Why not cut the rates now?

Jerome Powell: Well, we have a strong economy. Development is going on at a strong speed, the labor market is strong, 3.7% joblessness. With the economy strong like that, we seem like we can approach the concern of when to start to decrease rate of interest thoroughly. We wish to see more proof that inflation is moving sustainably down to 2%. We have some self-confidence because, our self-confidence is increasing. We simply desire some more self-confidence before we take that really essential action of starting to cut rate of interest.

Notification the declaration, ” We seem like we can approach the concern of when to start to decrease rate of interest thoroughly.” This is the old and sluggish part I have actually been going over considering that completion of 2022. The Fed currently has a limiting policy and if the labor market was breaking today they would be cutting rates strongly. Nevertheless, rather of getting ahead of the curve and leaving limiting area into neutral policy, they will take their time on this and remain limiting for a bit longer.

This has actually been a style of my work considering that 2022 and is why I prefer labor information over inflation information at this phase. Back in 2022, the Fed went over having the Fed Funds rate mirror 3, 6 and 12-month PCE information. Today, PCE three-month and six-month inflation is running listed below 2%, heading 12-month PCE is performing at 2.6%, core PCE 12-month is running at 2.9% and the Fed funds rate is over 5%.

With that sort of enhancement in inflation, why is the Fed running the risk of being limiting with its policy? It’s since they will feel much better about cutting rates when the labor market is breaking. The information line that will alter whatever is not more BLS tasks Friday reports like we simply had, however the out of work claims information. It is merely too low for the Fed to pivot.

We are visiting rate cuts this year. The Fed thought that policy was too limiting when the 10-year was near 5% and we had 8% home mortgage rates, however they appear great with home mortgage rates in between 6% -7.25% today. Here’s another quote from the 60 Minutes interview:

Pelley: The next conference around this table that will choose the instructions of rate of interest remains in this coming March. Understanding what you understand now, is a rate cut most likely or less most likely at that time?

Powell: So, the more comprehensive circumstance is that the economy is strong, the labor market is strong, and inflation is boiling down. And my coworkers and I are attempting to choose the best point at which to start to call back our limiting policy position.

This plainly reveals that the Fed hasn’t rotated now, they simply didn’t desire their policy to be too limiting. The last thing they desire on their plate is a job-loss economic crisis entering into an election year after they treked so high so quickly.

Bond yields respond

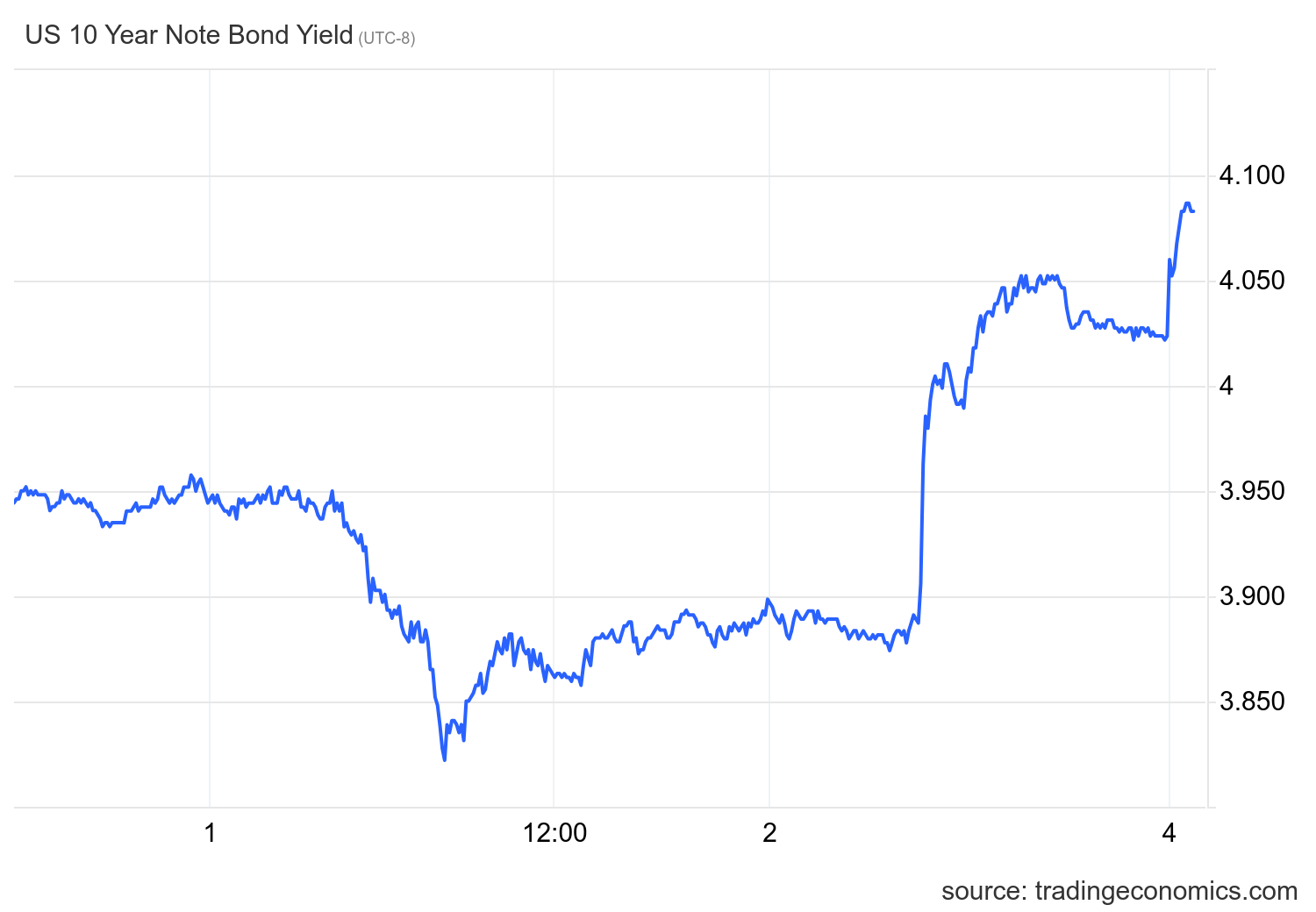

Let’s take a very first glimpse at the bond market response to the interview. The 10-year yield headed greater after this interview went live, increasing from 4.02% to 4.07%

The 10-year yield is the secret for real estate in 2024. In my 2024 projection, I set the 10-year yield variety in between 3.21% -4.25%, with a vital line in the sand at 3.37% If the financial information remains company, we should not break listed below 3.21%, however if the labor information gets weaker, that line in the sand– which I call the Gandalf line, as in “you will not pass”– will be evaluated.

This 10-year yield variety suggests home mortgage rates in between 5.75% -7.25%, however this presumes spreads are still bad. The spreads have actually been enhancing this year a lot that if we struck 4.25% on the 10-year yield, we will not see 7.25% in home mortgage rates.

Below is the chart of the 10-year yield considering that Feb. 1 and you can see the response after Powell talked on 60 minutes Sunday: yields went greater.

We remain in the upper-end variety of my 10-year yield projection, and out of work claims are near the historic bottom of the post-COVID-19 healing. My design is based more on claims information, so this looks about right.

What about real estate?

Powell didn’t talk about real estate at all in this interview and the Fed remains in a type of no-man’s land when speaking about real estate. The only silver lining I can state here for the real estate market is that if the Fed didn’t discuss a 5% 10-year yield and 8% home mortgage rates being too limiting with Fed policy. We may be there today after the last tasks report! That’s the most favorable spin I can draw from the current actions– that they understand they were pressing the limitations with the real estate market.

Keep in mind, a lot of economic downturns begin with losing property building and construction tasks so they bear in mind this truth in an election year.

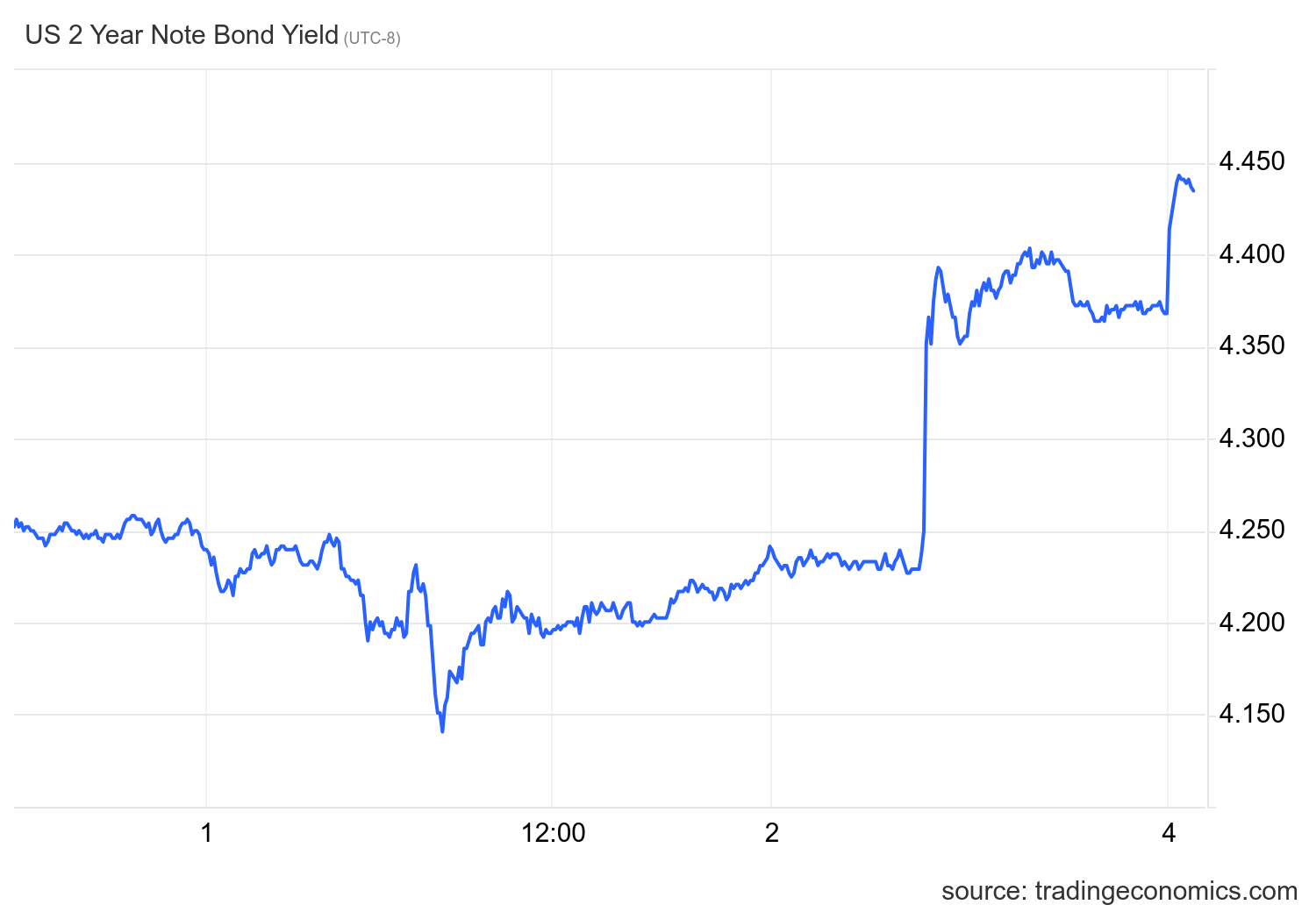

At this moment of the cycle, if you desire a concept on rate cuts, the 2-year yield is the very best location to go. I will persevere on getting no greater than 3 rate cuts in 2024 unless out of work claims get to 323,000 on a four-week moving average. Regrettably, if the Fed hasn’t rotated already it will be far too late. Today, the 2-year yield is increasing from current lows, making more aggressive rate cut projections not likely.

Like the 10-year, the chart of the 2-year yield listed below programs a strong response to the 60 Minutes interview.

Powell’s most current interview makes it clear: Absolutely nothing huge will alter over the next couple of months no matter what occurs with inflation– the labor market hasn’t broken enough for the Federal Reserve to pivot.